Resources

Welcome to the CFP Resources Page. Watch my video to find out what’s on the new Certified Financial Planner resources page.

Welcome. Let's get started.

Let’s look at an overview of what’s required.

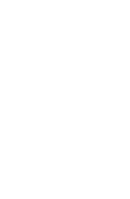

When should you buy the case study and get cracking on creating your financial plan?

You cannot progress on until you know that you have passed your L6 exam or obtained an exemption. You can then buy a case study from CISI. You then have 10 weeks to complete and submit your financial plan for assessment. There are quarterly windows during which time you can buy a case study from CISI.

You should think about the time commitment that you need to make to this. It is likely to take you in excess of 60 hours work! That's no picnic! Decide whether you want to buy your case study as soon as you receive your result (or exemption) or if you want to wait for the next quarterly window. Once you have passed your L6 exam there is no time limit on when you need to have started your L7 case study.

Lockie Consultants will be here to help you, whether you wait a quarter or two, or dive straight in after you receive your result.

Is this free content enough to pass the CISI L7 financial plan case study assessment?

No. The information contained on this website is designed to give you a flavour of things to think about in preparation for the work to come. It is not designed to be comprehensive. Please do not rely on this alone to pass your assessment.

What further support is on offer?

Lockie Consultants has two courses (use the links below to view the content):

Supported Learning Course: Comprehensive videos and instructional documents set out in a step-by-step way. Includes two 30-minute 1:2:1s and three 1-hour group calls. You will create your financial plan in your own time whilst following the course content. Numbers are limited and allocated on a first come first served basis.

CFP Fast Track Course: An intensive four-day live course with targets set each day of things that you need to complete to build your plan. With regular group check-ins during each day to keep you on track. We use a library of instructional how-to videos to help you build your spreadsheets. The aim is to have all your spreadsheets finished and for you to have started writing up your plan by the end of the course. With one post-course 1:2:1.

Click the BOOK A COURSE TODAY button below or the link here to view the full range of courses.

Let’s look at an overview of what’s required: Watch the video and take a look at CFP Part 1 below.

Getting started on your financial plan

Financial planning is like doing a giant 3D jigsaw puzzle. We are trying to get the best all-round fit for our clients’ objectives.

We need a mixture of hard facts and answers to additional questions that will add the colour we need about the clients’ objectives. In short, we need to ask great questions and listen to the answers.

Embarking on the CISI level 7 case study assessment is no easy feat. It isn’t meant to be. After all it is set at master’s degree level. I often say to my coaching clients that if were easy, everyone would do it and then there would be less value in it; a bit like doing your entry level 4 regulated exams.

Becoming a Certified Financial Planner professional allows you to do two things:

- To offer an excellent, robust and repeatable financial planning service for the long-term benefit of your clients and your business and

- To differentiate yourself from the growing crowd of people who call themselves ‘financial planners’ but who do not necessarily practice what we think of as financial planning.

Let’s look at an overview of what’s required:

Net worth and income and expenditure statements

You will be provided with a net worth and income tax calculations for the clients’ current situation. You need to become very familiar with them. Think about the following things:

- Who owns which asset?

- How is any property owned? If jointly, as joint tenants or tenants in common?

- Are there any one-off capital expenditures?

- Have the inflows arrived? If not, is it certain that they will arrive in the anticipated timescales?

- Is there an opportunity to change the ownership of assets? Is this consistent with the clients’ objectives and what are the consequences (good and bad)?

- Are there big credit card or other debts that might be worthwhile to pay off first?

You also need to be very familiar with how to calculate revised income tax and capital gains tax as necessary. For example, if you find that you need to increase a client’s pension contribution, whether by salary sacrifice or otherwise, this will affect the income tax calculation for that client. This will have a knock-on effect of potentially reducing the amount of net disposable income that the clients have to spend on other recommendations that you will make later in the plan. Consequently, if you cannot accurately alter the tax calculations to reflect this sort of change, learn that now.

Income tax

You also need to be very familiar with how to calculate revised income tax and capital gains tax as necessary. For example, if you find that you need to increase a client’s pension contribution, whether by salary sacrifice or otherwise, this will affect the income tax calculation for that client. This will have a knock-on effect of potentially reducing the amount of net disposable income that the clients have to spend on other recommendations that you will make later in the plan. Consequently, if you cannot accurately alter the tax calculations to reflect this sort of change, learn that now.

Let’s continue with the next section. Watch the video and take a look at CFP Part Two.

CFP Part Two

So onto the next section.

Structuring your financial plan

There are so many ways to go about financial planning; so many in fact that it can get very confusing where to start and to ensure you haven’t missed out anything important.

My suggested layout

This is not a defined requirement of the CFP case study, but I have found it a helpful structure to maximise your chances of passing the assessment. Feel free to choose your own layout of the plan if that suits you better.

Contents:

1. Introduction

2. Objectives/goals

3. Attitudes

4. Assumptions - Summary

5. Net worth statement comment

6. Income and expenditure comment

7. Cashflow planning, e.g. school fees, wedding, house deposit, retirement, long-term care planning

8. Personal risk analysis

9. Estate planning

10. Any other issues

11. Action plan

12. Reviews

Appendices:

1. Net worth statements

2. Income and expenditure statements

3. Revised tax calculations

4. Assumptions – Full explanations and reasoning

5. Cashflow funding calculations

6. Personal risk calculations

7. IHT calculations (pre-/post-recommendations)

calculations to reflect this sort of change, learn that now.

Can I use cashflow modelling software such as Truth or Voyant to create my financial plan for assessment?

Potentially, at least in part. There are a number of cashflow modelling tools available on the market at the moment. Some are definitely helpful. Outputs from others that I have seen have significant issues when it comes to using them for comprehensive financial planning. That might be because the financial planner is not good at using the software, as I just see the outputs, or it might be because the software has significant limitations. So, you need to be careful.

Let’s look at an overview of what’s required: Watch the video and take a look at CFP Part 3 below.

CFP Part Three - FP Assumptions

Let’s look at an overview of what’s required.

What assumptions are given to me with my case study?

You will be given the following assumptions:

- Price inflation

- Earnings inflation

- Investment growth rates for various asset classes

What assumptions do I need to create myself?

There will be other relevant assumptions you will need to complete the analysis. Only create and use the ones that are relevant to your clients. Don’t go creating ones that aren’t directly relevant! They might include:

- Expenditure escalation

- School fees escalation

- University fees escalation

- House price inflation

- Taxation

- State benefits escalation

- Health

- Longevity

- Fund costs

- Annuity rates

- Escalation of tax bands, allowances and exemptions

- Your fee for delivering this advice (note it can be zero if pro bono work)

CFP Podcast Series

We have several series of podcasts looking at all things Certified Financial Planner professional related. This one is all about assumptions.

CFP Part Four - Cashflow analysis

So onto the next section: Cashflow funding projections

Composite rate of return

We first need to be clear on what our clients’ attitude to risk are and if they differ over different time periods. Look up the information in your case study. Towards the back there should be a table that details how they feel about taking risk over different time horizons.

You then need to define an asset allocation breakdown for those specific risk profiles.

For example, if the client says that they are ‘modest risk’ over the long term, then you need to state, with reasons, what asset allocation percentages are appropriate for that period. I might say, for example, that in my business the mix for ‘modest risk’ would be 50% defensive + 50% growth assets The debt/equity distinction can be described as: debt is money you lend to someone (you get your capital back plus interest for its use) while equity is a share of an enterprise from which you may receive a share of earnings and you may find someone willing to buy the asset from you in the future based on their expectations of its future return. You are given defined rates of return for cash, fixed interest, property and equities. You therefore need to break down the asset allocation into which classes are defensive and which are growth and then break it down further to show the individual percentages, like this:

Defensive = 50%. Made up of Cash and fixed interest.

Growth = 50%. Made up of property (They behave like equities only insofar as they are priced daily by the market but their long term return will be closer to that of property than of businesses) and equities.

Asset allocation (as defined by me):

Cash 20%

Fixed interest 30%

Property 10%

Equities 40%

NOTE: if you disagree with what I’ve said about property as an asset class and believe it should be in the defensive category, then that’s fine. You just need to write a valid reason either way. The next step is to apply these percentages to the given rates of return, add them up and you get a composite rate of return.

Asset type | My asset allocation percentage | *Rates of return given by CISI | Calculation | Composite rate |

|---|---|---|---|---|

Cash | 20% | 2% | 20% x 2% | 0.4% |

Fixed interest | 30% | 3% | 30% x 3% | 0.9% |

Property | 10% | 5% | 10% x 5% | 0.5% |

Equities | 40% | 6% | 40% x 6% | 2.4% |

Total | 100% | 4.2% |

*note: check the rates you are given with your case study

Remember that this rate makes no allowance for inflation and so if you are running your spreadsheets in real (as opposed to nominal) terms, you need to follow the Fisher equation I talked about in the assumptions video to remove inflation from this figure.

Discounting back for school fees

We can now apply this rate in several areas. One is for the school fees planning.

- Using the spreadsheets shown in the video (see the homework section for links to brush up your knowledge if needed) to calculate the total amount of money needed in each year. Make sure you increase that in line with whatever you’ve chosen for your school fees escalation rate. You will end up with one capital amount for each year.

- Add them all up to get the total capital that’s needed over the entire term.

- Discount this total back to today using your composite growth rate.

- That will give you the amount that needs to be invested today assuming that you earn that return throughout the term. If your assumed growth rate is positive, the answer should be less than the total over the entire term. Look back at the video to see how to set it all out.

Retirement planning

This section is much more complex than the school fees but the principles are the same. You need to show:

- calculations for the composite rate of return for the retirement planning strategy. Do this by repeating the steps above but look at the clients’ information in the case study for ‘retirement risk tolerance’. Don’t mix it up by using the school fees rate if their attitude to risk is different for the two objectives.

- whether the current asset allocation of their existing pensions is suitable? If not, make a note to change them to align with your recommended allocation and its associated composite rate of return.

- how far the current pension (and/or other assets currently being allocated to retirement planning) are away from the clients’ stated objective.

- a cashflow showing all the retirement money going in and out to meet the clients’ objective, starting at the date they specified.

- state benefits in the year/s when they are due to start – age 67+ probably.

Don’t mix up real and nominal information in your spreadsheet – e.g. if you are running your numbers in real terms and you state in your assumptions that state pensions will go up in line with the same measure for price inflation, then the value for the state pension on your spreadsheet will remain unchanged. This is because you are showing values net of inflation.

Make sure you include personal allowances and the resulting tax that might need to be paid. Remember the amount that the clients stated that they want to spend is NET DISPOSABLE INCOME, so it is net of taxes. It may be more effective to provide cashflow from other sources. Look at the example in the video and the sample plan which is in your candidate guidance.

You will be able to tell by the end just how much needs to be paid into each client’s pension pot or other suitable investment wrapper to meet their stated objectives.

What happens if you run out of money when doing the analysis and some of the clients’ objectives cannot be met?

You have three options:

- Can the clients cut back their expenditure in any obvious way?

- Can the clients take more risk? Probably not likely.

- Can the clients extend their time horizon to meet this particular objective? Not always possible for things like paying school fees but may be possible for retirement.

If all that is difficult then look back at the analysis again because you might have made a mistake! You might need to rethink your earlier proposed solutions. You CANNOT just say, “Sorry, you’ve run out of money!” You must find a way around these issues to make the solutions to all the objectives achievable.

CFP Podcast Series

This episode looks at the common problems that the case study assessors see so you can avoid them!

CFP Part Five - Personal risk analysis

Let’s look at an overview of what’s required. Protection and personal risk analysis.

Review the existing assets

You need to take into account any income that might be generated by investments that are NOT being used for school fees or retirement planning. What more do they have? Don’t ignore other income-producing assets as they will generate some income or capital to help mitigate at least some of the likely income shortfalls.

Do not over insure your clients!

If your calculations show that you have a shortfall of £20,000pa do not insure for £30,000pa without an EXTREMLY good reason and a clear explanation. I regularly see existing bank accounts with sizeable balances ignored and more insurances recommended. DON’T DO THIS! You can easily cause other knock-on effects for your client later down the line. For example, I have seen an excess income of £40,000pa generated but the planner did not spot that this amount would cause a large and growing IHT problem that the client’s stated that they wanted to mitigate! You should think through what you are recommending and what effects there might be in later years. A lifetime cashflow can be helpful here as it allows you to visualise the future.

Think through what happens when a term assurance policy stops

If you use a family income benefit policy to plug a potential gap, that is fine but you must consider what happens to the cashflow when that policy stops paying out. You might be covering the life of one of the client’s easily but depending on the age of the other, they might have an income shortfall if one client dies and then the policy stops paying out further down the line. Watch out for that.

Let’s continue with the next section. Watch the video and take a look at CFP Part Six.

CFP Part Six- Estate planning analysis

So onto the next section: Estate planning

Think through the ramifications

Now you should be able to see where there are estate planning issues. By ‘estate planning’ I don’t just mean IHT issues! Think about what happens to the estate when one or other client dies. Are you recommending potentially exempt transfers (PETs)? Maybe there are chargeable lifetime transfers (CLTs) too? What happens to the estate value where CLTs are involved?

Look back over your plan with your estate planning goggles on!

Review the recommendations you plan to make and check how they affect the estate planning aspects. You might find that your calculations are fine but the ownership of some assets might need tweaking in order to achieve the same outcome for the earlier objectives. But the revised ownership might be a better all-round solution to mitigate IHT as well.

Leave enough space and time

It is easy to think that the estate planning section might not take very long to produce. However, do not underestimate how your solutions might interfere with recommendations that you have already made. This section will also take up more than the commonly two or three pages that most people seem to have available when they get this far in the creation of their financial plan. If that happens, you will likely fail this section so you’ll need to go back to the earlier sections and cut them back a little.

CFP Podcast Series

We speak to Alasdair Walker CFP™ MCSI FPFS, Managing Director, Handford, Aitkenhead and Walker, who recently gained his CFP certification in the UK.

CFP Part Seven - Finishing your financial plan

So onto the final section.

Writing up your financial plan

Your financial plan needs to be written to the clients, NOT to the assessors. It should NOT include reference to the CFP assessment standards. Write it as you would normally present it. You have all the analysis and solutions now, you just need to walk the clients through the situation and your proposed solutions. Keep it short and don’t waffle! Do not use bullet points to replace whole paragraphs. If you have exceeded the maximum page limit, then you need to revisit the entire plan to cut it back a little.

Action plan

Do NOT put everything in your action plan as urgent or to be done ASAP! There will be some things in your financial plan that will need doing more urgently than others. Think through what they are and list them with shorter deadlines. You need to set out WHAT action needs taking, WHO needs to carry that out and by WHEN does each action need to be completed.

What happens if you cannot finish your financial plan?

You have two choices:

- Send what you have, knowing obviously that you will not pass this submission attempt. However you will receive feedback on what you’ve written and you’ll have another 12 weeks to resubmit it with changes.

- Do not submit it. If you miss the assessment deadline completely and don’t send anything in, you will need to start again and buy a brand new case study from CISI. The case studies are released every quarter. See CISI website for those dates.

What happens if you are unsuccessful with your submission?

You will receive a feedback letter from the CISI with comments from the CFP assessor on where you’ve gone wrong. Remember that, having put in a lot of work on your plan, you might be upset and you can easily misinterpret the feedback. Read it again when you are calmer to understand exactly what you are being told. DO NOT think that just by fixing exactly what the assessor tells you it will be all you need to do to pass. This is because the issues highlighted and resulting changes that you make may have a knock-on effect on other parts of your plan. You could accidentally make other recommendations unsuitable or unaffordable. For example, if you change an assumption, it can affect every other element of the plan.

What to do next?

If you have been unsuccessful in your CFP submission we can help you with individual 1:2:1 coaching to identify where things went wrong and help you make a plan to tackle those issues.